For fifteen years, one unwritten rule made a lot of people rich without them ever understanding why: whenever markets fell hard enough, the Federal Reserve would ride in with rate cuts and cheap money. Traders gave it a name — the “Fed put” — because it worked like a free insurance policy under your portfolio. Buy the dip. Cuts are coming. The Fed has your back.

Here’s the contrarian truth almost no one has repositioned for: in 2026, that insurance policy has been quietly cancelled. The market is no longer pricing rate cuts to rescue you. It’s pricing rate hikes — into a stock market that sits at the second-richest valuation in history. The single most important change to wealth-building this year isn’t a hot stock or a new coin. It’s that the safety net under the entire market has been removed, and most portfolios are still built as if it’s 2021.

The reflex that no longer works

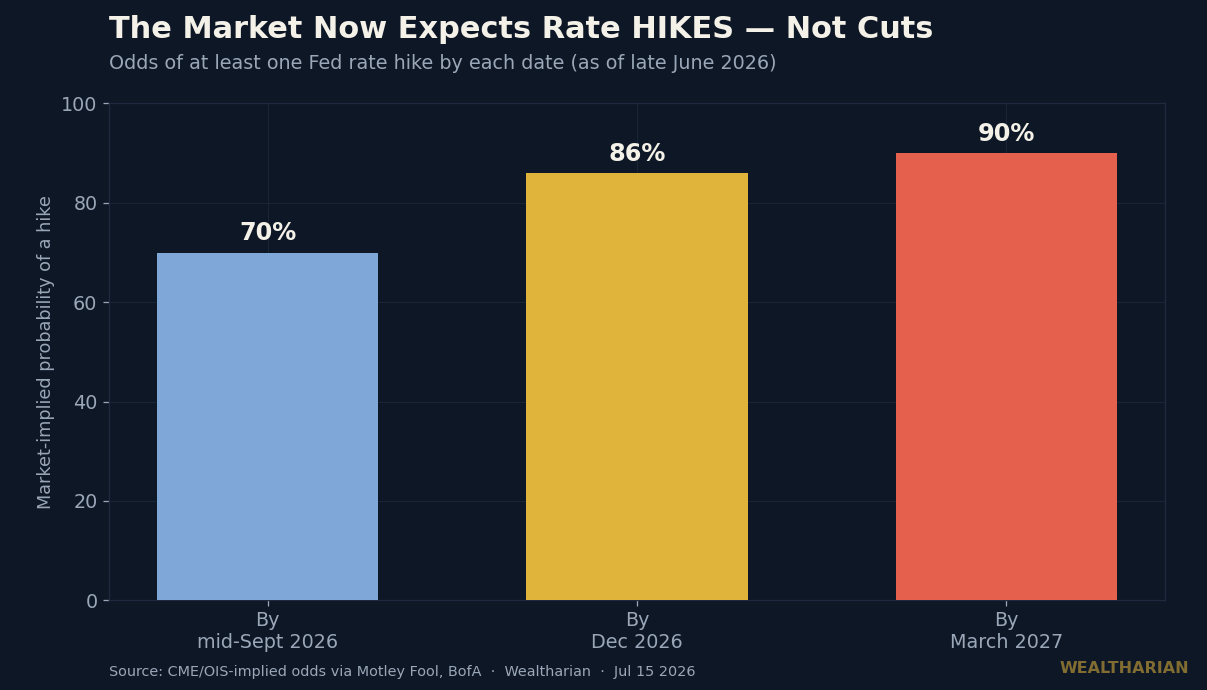

Under new Chairman Kevin Warsh, the Fed has dropped its easing bias entirely. This isn’t subtle. Bank of America now forecasts three rate hikes in 2026, lifting the benchmark from today’s 3.50%–3.75% toward 4.25%–4.5%. Market-implied odds tell the same story: roughly a 70% chance of at least one hike by mid-September, ~86% by December, and ~90% by March 2027. Warsh’s own committee raised its 2026 PCE inflation projection to 3.6%, up from 2.7% — an admission that price pressures are stickier than the “transitory” crowd promised.

Sit with that. For most of the last 15 years, the base case whenever stocks wobbled was “cuts are coming.” The base case now is the opposite. The buy-the-dip reflex that has been trained into an entire generation of investors — the muscle memory that says a selloff is always a gift — is running against the actual direction of policy for the first time in a very long time.

This matters because reflexes are expensive when the regime flips. The people who got hurt worst in past turns weren’t the ones who didn’t own stocks — they were the ones who kept doing the thing that used to work long after it stopped working. A rescue you’re counting on that never comes is more dangerous than no rescue at all.

Why a dead Fed put is so dangerous right now

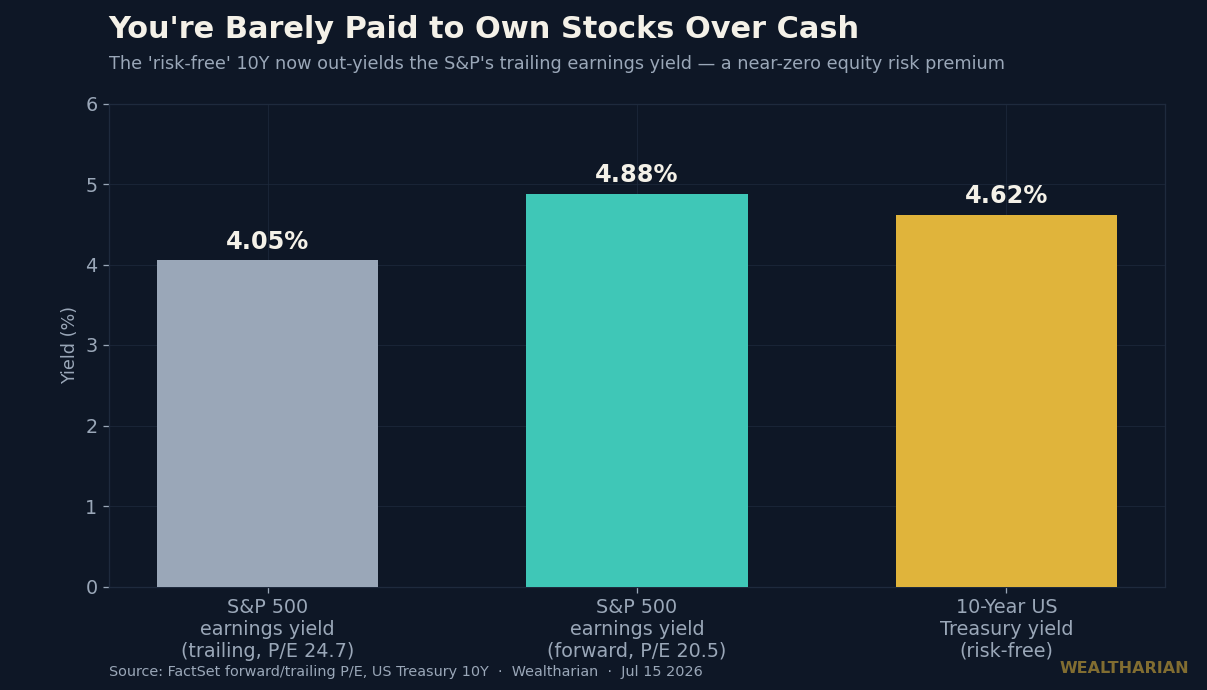

A hawkish Fed is survivable when stocks are cheap. The problem is stocks aren’t cheap — they’re historic. By trailing earnings the S&P 500 trades near a P/E of 24.7, and on forward estimates around 20.5 — above both the 5-year (19.9) and 10-year (19.0) averages. By several measures this is the second-most-expensive market in American history, behind only the dot-com peak. It’s no accident this is landing just as American households sit at record stock-market exposure — the all-in bet and the vanishing safety net are arriving together.

High valuations aren’t a timing signal — expensive markets can stay expensive for years. But they are a fragility signal. Rich multiples are only justified by cheap money and the expectation of more of it. Pull the cheap-money assumption away, and the same earnings are suddenly worth less, because every future dollar of profit gets discounted at a higher rate. A dead Fed put doesn’t just remove the rescue — it removes the core assumption holding today’s valuations up.

Cash finally pays you to wait

Here’s the part that should reframe how you think about risk in the second half of 2026. The 10-year Treasury now yields around 4.62%. The S&P 500’s trailing earnings yield — the inverse of that 24.7 P/E — is roughly 4.05%. Read that again: the “risk-free” government bond currently out-yields the earnings the entire stock market is generating.

That gap is called the equity risk premium — the extra return you demand for taking stock-market risk over sitting in safe assets. Right now it’s near zero, and by the trailing measure it’s negative. For fifteen years cash paid nothing, so there was no alternative to stocks — the famous “TINA” trade, There Is No Alternative. That era is over. Cash and short Treasuries now pay 4–5% while you wait, with none of the drawdown risk — and as we argued in where to put your cash in 2026, that window won’t stay open forever. The opportunity cost of being patient and liquid has collapsed to almost nothing.

This is the quiet revolution most portfolios haven’t absorbed. When you were paid 0% to hold cash, going all-in on expensive stocks was rational. When you’re paid 4.6% to hold a risk-free bond that out-yields those same stocks’ earnings, refusing to hold any dry powder is just a bet that the old reflex still works.

What to actually do with this

None of this is a case for panic-selling or for calling a top — market timing wrecks more wealth than bear markets do, and the death of the Fed put has been declared prematurely before. It’s a case for repositioning the assumptions your plan is built on. A few concrete shifts worth thinking through:

Get paid to be patient. With T-bills and money markets yielding 4–5%, holding a meaningful cash buffer is no longer a drag on your returns — it’s a paid option on future opportunity. Dry powder used to cost you; now it pays you while it waits.

Own the earnings, not the multiple. In a world where multiples can’t count on falling rates to lift them, returns have to come from real, growing cash flows. Favor businesses that compound earnings on their own, at prices where you’re not paying 25x for the privilege — over story stocks whose entire case is “the multiple goes higher.”

Stress-test your plan against a rescue that never comes. If your strategy quietly assumes the Fed will cut the moment things get ugly, it’s built on a policy stance that no longer exists. Ask the uncomfortable question: does my plan still work if the next move is a hike and the next drawdown has no cavalry behind it?

Come back to the one number that always wins. When returns get harder and cheap leverage disappears, the boring lever matters more than ever — how much you save and how little you owe. As we’ve shown before, your savings rate beats your returns; in a higher-for-longer world, that and your freedom from expensive debt do more for your net worth than any clever trade.

The death of the Fed put isn’t the end of wealth-building. It’s the end of the easy version — the one where a rising tide and a friendly central bank covered for undisciplined portfolios. The people who build real wealth over the next few years won’t be the ones waiting for a rescue that isn’t coming. They’ll be the ones who noticed the safety net was gone while everyone else was still trading like it was there.

The Fed just stopped being on your side. The question is whether your portfolio has caught up to that fact — or whether it’s still buying every dip, waiting for a phone call that isn’t going to come.

Want to track your own path to financial independence? The Wealtharian Wealth Tracker lets you monitor your net worth, FU money progress, and investment milestones in one place. Try it free →