For three years, the entire AI trade has rested on one question: who makes the best chip? That question is about to matter far less than almost anyone is positioned for. The real ceiling on artificial intelligence in 2026 isn’t silicon. It’s the wall socket.

Here’s the uncomfortable truth the chip-obsessed crowd keeps skating past: you can buy all the GPUs you want, but if you can’t plug them in, they’re paperweights. The AI power bottleneck — not compute — is now the binding constraint on the most important technology of the decade. And that single shift quietly rewrites where the next trillion dollars of wealth is going to land.

The Numbers Nobody Wants to Sit With

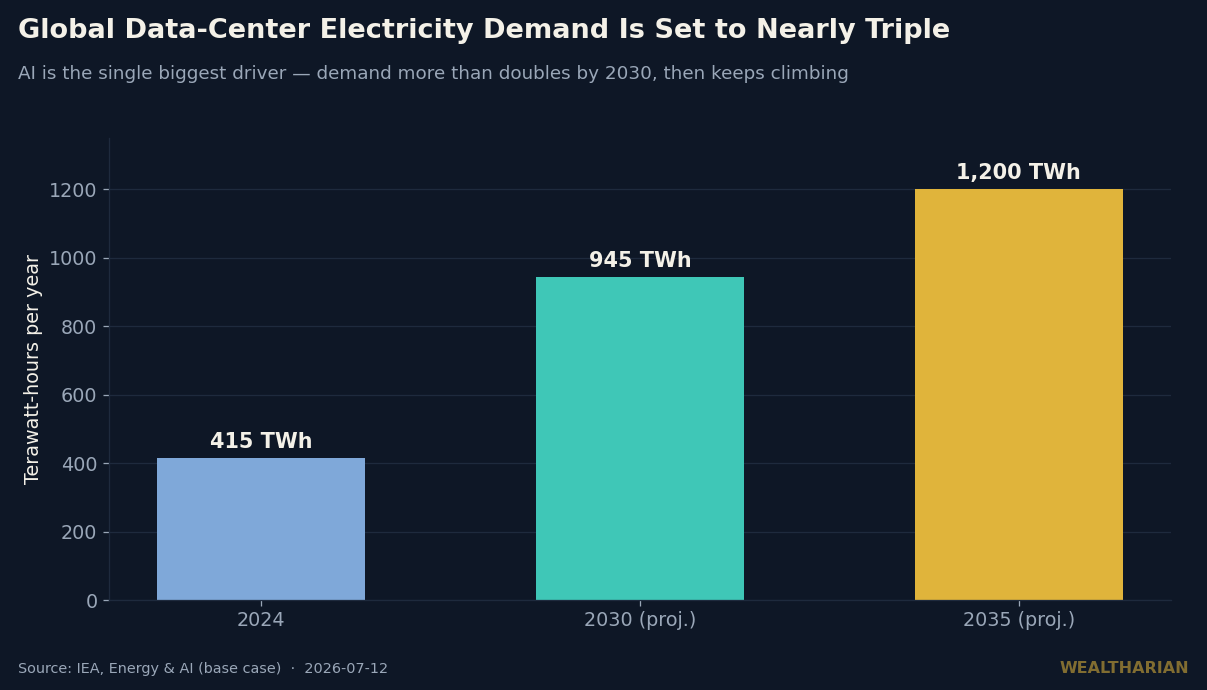

Start with the demand curve. Global data centers consumed roughly 415 terawatt-hours of electricity in 2024 — about 1.5% of all the power on Earth. The International Energy Agency projects that figure more than doubles to around 945 TWh by 2030 and keeps climbing to 1,200 TWh by 2035. The IEA is blunt about the cause: AI is “the most important driver of this growth.”

To put 1,200 TWh in perspective, that’s more electricity than entire industrial nations use today, consumed by buildings full of chips that didn’t meaningfully exist a decade ago.

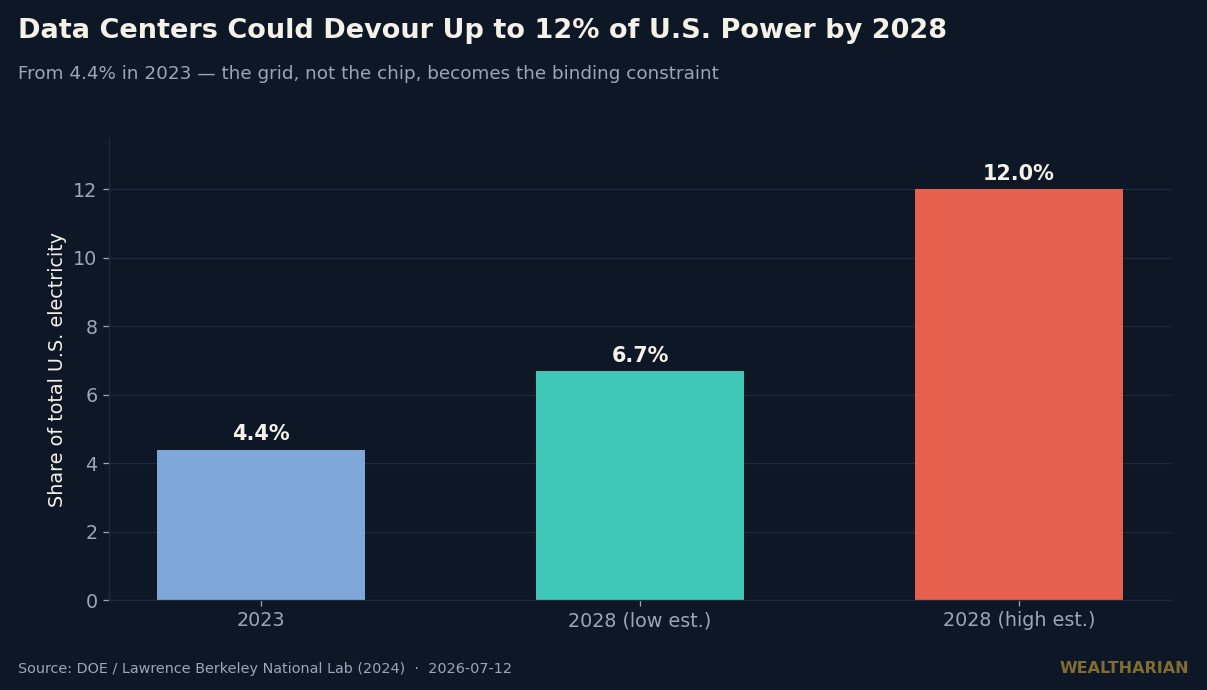

Now zoom into the United States, which already accounts for 45% of global data-center power use. In 2023, U.S. data centers ate about 4.4% of the country’s total electricity. By 2028, the Department of Energy’s Lawrence Berkeley National Lab projects that share hits somewhere between 6.7% and 12%. The high end means one out of every eight electrons in America runs an AI model.

A single large AI data center now pulls 100 to 300 megawatts — the same draw as 80,000 to 250,000 homes. New sites are being designed for a full gigawatt. That is not an IT problem anymore. It is a power-generation problem wearing an IT costume.

Why the Grid — Not the Chip — Is the Real Wall

The chip shortage was always going to be temporary; you can build more fabs. Power is different, and this is the part the market is mispricing.

Electricity can’t be shipped overnight from Taiwan. A new grid interconnection in the U.S. can take up to four years. Baseload generation — the always-on power AI needs, since a training run can’t pause when a cloud passes over a solar farm — takes even longer to bring online. Gartner now estimates that power shortages will physically restrict 40% of AI data centers by 2027. Read that again: not restrict revenue, restrict operation. The compute exists. The electrons don’t.

This is why the smartest capital in the AI buildout has quietly stopped asking “which chip?” and started asking “whose power?” Microsoft is bankrolling the restart of Three Mile Island. Meta signed long-term nuclear deals. Data centers are ordering gas turbines to generate power on-site — “behind the meter” — because they refuse to wait four years for a utility hookup. The buildout is being rerouted around the grid entirely. It’s the same dynamic we flagged when the AI boom shifted from cash to credit in the AI infrastructure debt boom: the real signal keeps moving to the part of the stack nobody is watching.

The Contrarian Wealth Angle

Here’s where most investors are making a subtle, expensive mistake. They think they own the AI energy theme because they own the chipmaker. They don’t. They own the part of the value chain with the most competition, the highest expectations, and the least scarcity.

The scarce asset in AI right now is not a transistor. It’s a megawatt of firm, dispatchable, near-term power. And scarcity is where durable wealth is built. When everyone is bidding for the same obvious asset, the return migrates to the bottleneck nobody wanted to underwrite. If chips get cheaper and more abundant — the exact trend behind the AI cost collapse — then power, not silicon, becomes the line item that decides who wins.

Follow the actual constraint and a different map appears. Independent power producers with existing nuclear fleets — the Constellations and Vistras of the world — are suddenly sitting on the one thing money can’t quickly manufacture: gigawatts that already exist and run 24/7. Vistra is buying up gas capacity across the biggest power markets. GE Vernova, which makes the turbines data centers are now ordering to bypass the grid, saw orders jump 71% year-over-year and sits on a record backlog north of $160 billion. That backlog is a customer list of people who decided power was worth more than patience.

None of this is a recommendation to chase any single ticker — several of these names have already run hard, and buying a good story at a bad price is how people lose money in every boom. The point is structural: the AI trade is quietly becoming an energy trade, and most portfolios haven’t noticed. The wealth doesn’t necessarily flow to the flashiest layer. It flows to the layer that can say no — the one holding the resource everyone else needs and can’t quickly replace. It’s the same lesson as every crowded trade: the edge lives where the crowd isn’t looking.

There’s a genuinely good story underneath the money story, too. To feed AI, the industry is being forced to fund the biggest expansion of clean, reliable power — especially nuclear — in two generations. That grid gets built for data centers, but it stays for everyone: hospitals, factories, homes, EVs. This is the rare case where the wealth thesis and the human-progress thesis point the same direction. A stronger grid is good for your country and, if you’re positioned right, good for your net worth.

How to Actually Position

Three practical moves, in plain terms. First, stop treating “AI exposure” and “chip exposure” as the same thing — audit whether your AI bets are all sitting in one crowded layer. Second, study the whole stack: generation (nuclear, gas), the equipment that delivers it (turbines, transformers, grid gear), and the utilities in the regions where data centers are actually landing. Third, respect valuation — the thesis can be right and the entry price can still be wrong, so let the bottleneck, not the hype, guide what you pay.

The crowd is still arguing about whose chip is fastest. The quiet winners of this decade may be the least glamorous companies imaginable — the ones that keep the lights on.

Want to track your own path to financial independence? The Wealtharian Wealth Tracker lets you monitor your net worth, FU money progress, and investment milestones in one place. Try it free →