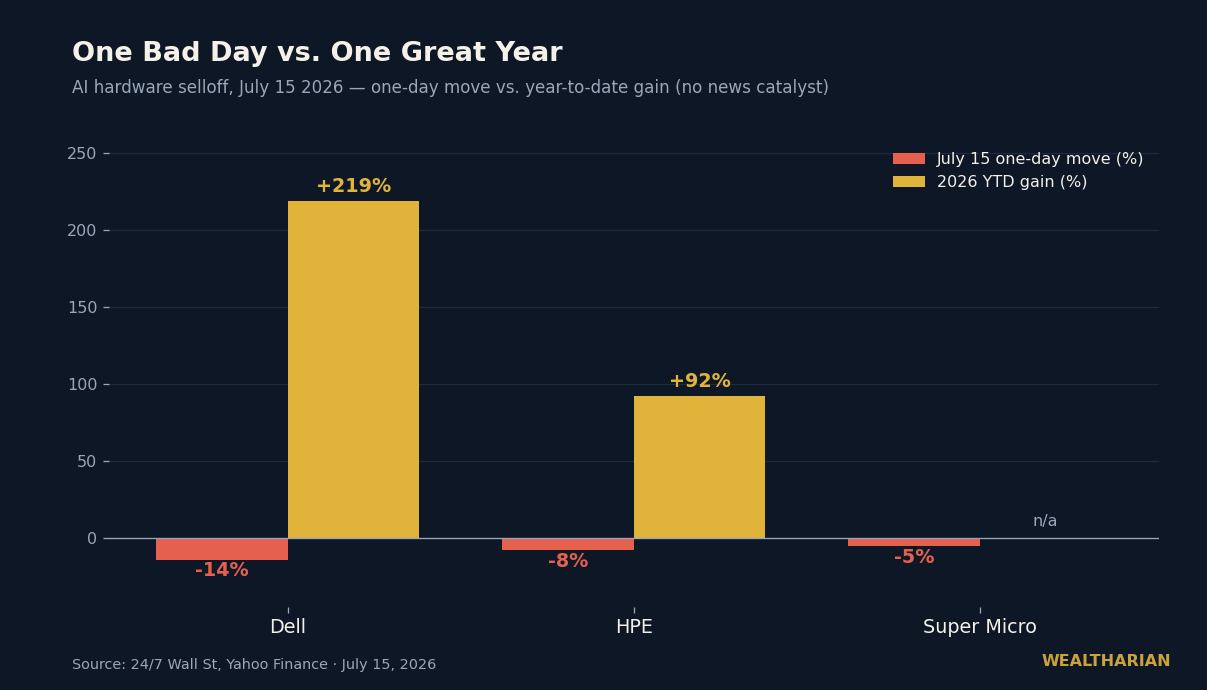

On Tuesday, Dell lost roughly $37 billion of market value in a single session — a 14% one-day crash — on no earnings report, no guidance cut, no news at all. The same day, ASML, the Dutch company that builds the machines that make AI chips possible, raised its full-year forecast for the second time this year, and Apple hit an all-time high.

If you’ve been following the standard advice — “don’t chase the AI hype, buy the AI picks and shovels” — that split-screen should bother you. Because Dell, HPE, and Super Micro are the picks and shovels. They build the servers every AI data center runs on. Their order books are overflowing. And the market just repriced them anyway. Here’s the contrarian truth: the picks-and-shovels playbook is the most misused piece of investing advice of this cycle, and Tuesday was the market telling you exactly why.

A split-screen day

The numbers first. Dell fell 14%. Hewlett Packard Enterprise fell 8%. Super Micro fell 5%. No catalyst, no downgrade-triggering event — just a sudden, violent rethink. And this wasn’t a bear raid on losers: even after the drop, Dell is still up 219% year-to-date and HPE up 92%. These were two of the best-performing large caps of 2026.

Meanwhile, on the very same tape: ASML raised its 2026 outlook to €43–45 billion in sales on booming AI chip demand — its biggest guidance raise of the year. Amazon, Alphabet, and Microsoft each gained around 3%. Apple printed a fresh all-time high. Even the macro backdrop was friendly: June CPI fell 0.4%, core inflation came in at 0.0% month-over-month, and the odds of a Fed hike on July 29 collapsed from 42% to 17% in a day. A cooling-inflation, risk-on session — and the AI hardware names still got crushed.

So this wasn’t “AI is over.” AI infrastructure demand is accelerating. What cracked was something more specific — and far more useful to understand.

The AI picks and shovels lie

Everyone knows the gold-rush story: the miners mostly went broke, while the people selling picks, shovels, and jeans got rich. The lesson investors took from it — own the suppliers, not the dreamers — is fine as far as it goes. We’ve argued the picks-and-shovels case ourselves in our piece on the AI bubble reckoning. But the mantra skips the part that actually made Levi Strauss rich: he wasn’t rich because he sold to miners. He was rich because nobody else could sell what he sold.

That’s the distinction the market enforced on Tuesday. Not all shovel-sellers are equal:

Some “shovel” businesses are chokepoints. ASML has a literal monopoly on the EUV lithography machines that advanced AI chips require. TSMC manufactures the overwhelming majority of leading-edge chips on Earth. Nvidia designs the accelerators everyone still queues for. If you want what they sell, you pay what they charge.

Other “shovel” businesses are assembly lines. Dell and HPE buy Nvidia’s chips, buy memory, buy power supplies, bolt them into racks, and ship them — in competition with Super Micro, Foxconn, and every other integrator bidding for the same hyperscaler contracts. The product is essential. The seller is replaceable. That is a logistics business wearing an AI costume.

Margin is the map

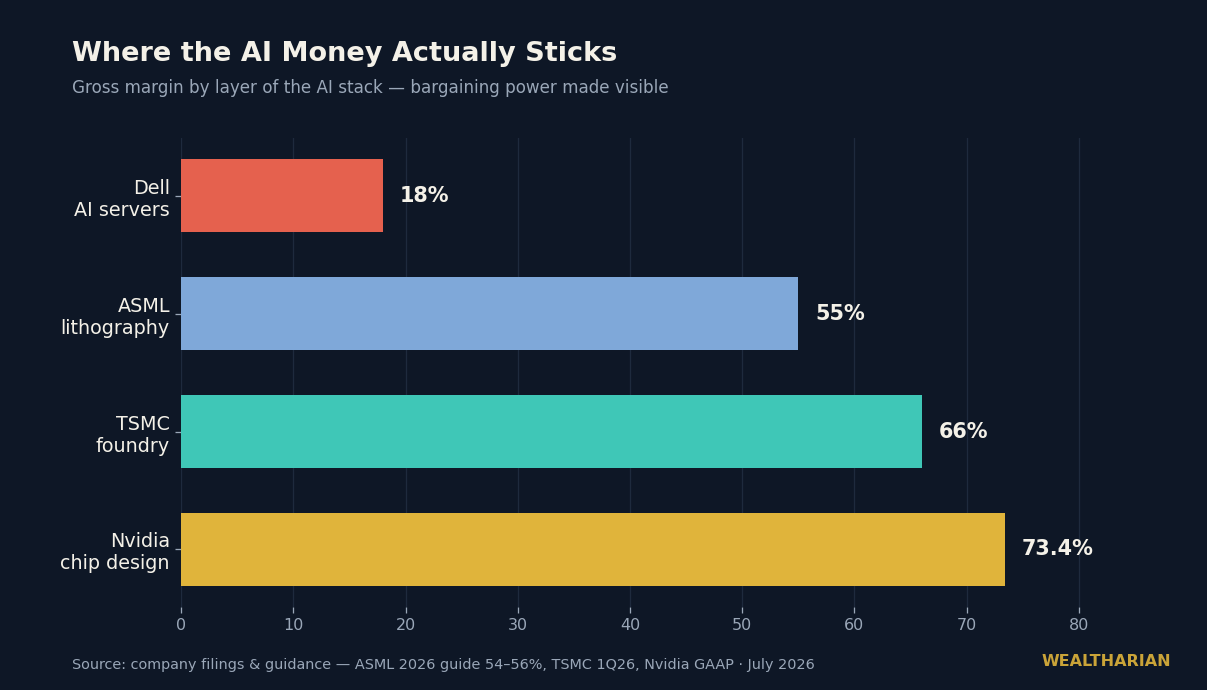

How do you tell a chokepoint from an assembly line? You don’t need inside information. You need one number: gross margin. Gross margin is bargaining power made visible — it’s the share of every sale a company keeps because customers have nowhere else to go.

Look at the AI stack through that lens: Dell’s AI server business runs gross margins around 18%. ASML guides 54–56%. TSMC just printed 66%. Nvidia runs 73.4%.

Same boom. Same customers. Same “picks and shovels” narrative. And a four-times difference in how much wealth each layer keeps from every dollar flowing through it. Dell’s problem was never demand — Q1 revenue grew 88% year-over-year, and the company guides to $60 billion of AI server revenue in FY27. Dell’s problem is that revenue is not wealth. Analysts spent the week flagging rising memory and component costs squeezing that thin 18% even thinner, and there’s nothing Dell can do about it, because its suppliers have pricing power and Dell doesn’t. When input costs rise, Nvidia passes them on. Dell absorbs them.

The wealth rule underneath this is old and brutally reliable: in every boom, value pools at points of scarcity, not points of activity. The busiest layer of a supply chain is often the poorest. The railroads moved the goods; Carnegie owned the steel. Everybody built websites in 1999; the money went to whoever owned the routers, then the platforms. Everyone is “in AI” in 2026 — the question that decides returns is who owns something scarce.

What this means for your money

First: stop reading revenue growth as a buy signal. Growth tells you a market is real. Margin tells you who captures it. An 88% revenue grower on 18% gross margins can be a worse business than a 20% grower on 70% margins — and the market will eventually price that, violently, on a random Tuesday.

Second: recognize a positioning unwind when you see one. A stock that’s up 219% on the year does not drop 14% on zero news because its business changed overnight. It drops because a crowded trade got tapped on the shoulder. High-beta AI hardware became the default “safe” way to play AI, everyone owned it, and when the first holders headed for the door, there was no incremental buyer left. If your thesis for owning something is “everyone knows this is the smart AI play” — that’s not a thesis, that’s a queue.

Third: notice that the boom didn’t break — it’s concentrating. On the day hardware assemblers were dumped, the market paid up for the monopoly toll booths and the platforms. That’s not a market losing faith in AI. That’s a market getting more discriminating about who actually gets to keep the money — which is what happens in the middle of every real technology buildout, and it’s healthy.

We made a related argument in yesterday’s piece on the death of the Fed put — the era of cheap money bailing out every crowded trade is over, which makes margin quality matter more, not less. And if the lesson feels abstract, it’s the same one that applies to your own finances: what you keep beats what you make, in portfolios and in paychecks.

The bottom line: “Buy the AI picks and shovels” was never wrong. It was incomplete. Buy the picks and shovels nobody else can make — and be very suspicious of any business whose entire pitch is standing between a monopolist and a customer.

Want to track your own path to financial independence? The Wealtharian Wealth Tracker lets you monitor your net worth, FU money progress, and investment milestones in one place. Try it free →