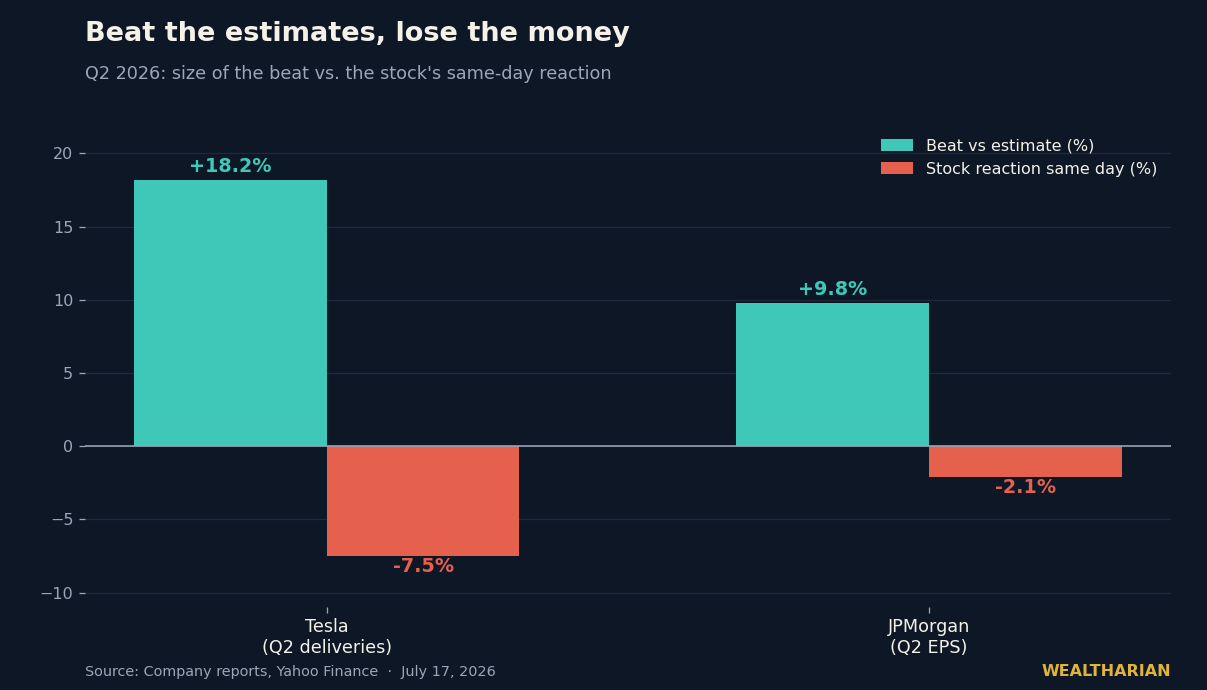

On July 2, Tesla reported 480,126 quarterly deliveries — 18% above what Wall Street expected. The stock fell 7.5%, its worst day in a year. Last week, JPMorgan beat earnings estimates by nearly 10% and dropped anyway. Welcome to the strangest earnings season in years: the numbers are spectacular, and the market doesn’t care.

If your portfolio strategy is “own great companies that beat expectations,” this season is quietly breaking it. The market you’re investing in right now is priced for perfection — and understanding exactly what that means, in numbers, is the difference between compounding through the next 12 months and donating your gains to someone who read the tape better.

The beat-and-drop tape

Start with how good the earnings actually are. Of the early S&P 500 reporters this season, 88.9% beat EPS estimates — against a consensus that already called for roughly 23.6% year-over-year earnings growth, one of the strongest projections of the cycle. Even more unusual: analysts raised Q2 estimates by 3.4% during the quarter itself. In a normal quarter, estimates drift down 2–3% as companies guide expectations lower so they can “beat.” This quarter, the bar rose the whole time — and companies still cleared it.

And yet: Thursday the S&P 500 fell 0.51% and the Nasdaq dropped 1.47% — on a day when 87% of reporters had beaten estimates, producer prices unexpectedly fell 0.3%, and jobless claims came in better than expected. Good macro, great earnings, red tape.

The single-name examples are brutal. Tesla’s delivery beat was enormous — 480,126 vehicles against 406,024 expected — and the stock was executed for -7.5%. JPMorgan posted $6.14 in adjusted EPS against a $5.59 consensus, a 9.8% beat, and fell more than 2% because management nudged its expense outlook higher. TSMC beat earnings, raised its revenue outlook, and raised its capex plans — and the entire semiconductor complex sold off, because higher spending means someone has to earn a return on it.

Expectations are the price

Here’s the mental model most investors never install: when you buy a stock, you are not buying a company — you are buying the gap between the company’s future and the expectations already embedded in the price. The company can be magnificent. If the price already assumes magnificence, you own the gap, and the gap is zero.

That’s what “priced for perfection” means mechanically. The S&P 500’s forward P/E has run above its 10-year average for most of this year. A high multiple is not just “expensive” — it is a precise statement about the future: it says earnings must not only grow, they must grow faster than the already-optimistic consensus, indefinitely, without accidents. Beating estimates stops being an achievement and becomes the minimum entry requirement. The applause is pre-spent.

This is the same lesson the market taught on Tuesday, when Dell — a company growing AI server revenue 88% a year — lost $37 billion of market value in a session. We covered that anatomy in The AI Picks-and-Shovels Trap: value doesn’t pool where the activity is, it pools where the scarcity is. This week’s sequel: returns don’t pool where the earnings are, they pool where the expectations gap is.

The punishment curve

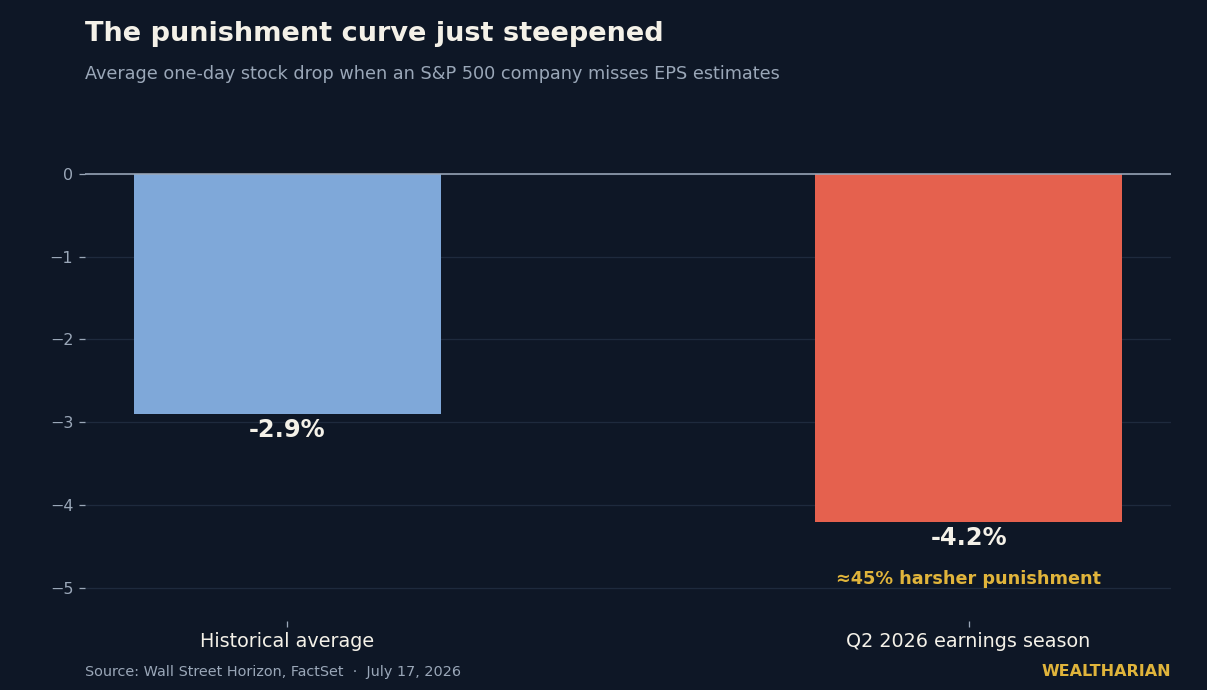

There’s a number that captures this season better than any other. Historically, when an S&P 500 company misses earnings estimates, the stock falls about 2.9% on average. This quarter, missers are falling 4.2% — roughly 45% more punishment for the same crime.

Meanwhile the reward for beating has compressed toward zero — and in the Tesla and JPMorgan cases, gone negative. Asymmetry like this is not noise. It’s the market telling you, in its own language, that positioning is crowded, valuations are full, and the marginal buyer is exhausted. When beats get shrugged off and misses get executed, the risk-reward of “just own the winners” quietly inverts: your upside is capped by expectations and your downside is amplified by them.

Notice what this is not saying. It’s not saying a crash is coming. Earnings growth of 23%+ is real wealth creation, the consumer is still spending — June retail sales rose for a fifth straight month, up 6.7% year over year — and inflation is genuinely cooling. The economy is fine. The prices are the problem.

The expectations playbook

First: stop grading companies and start grading expectations. Before you buy anything, ask the only question that matters: what does the current price already assume? A rough shortcut: a forward P/E of 30+ assumes near-flawless execution for years. If your answer to “what could go better than expected?” is just “more of the same,” you own no gap.

Second: hunt where expectations are on the floor. The mirror image of Tesla falling on record deliveries is an asset falling so far out of favor that mediocre news becomes a positive surprise. Consider the sentiment extreme in crypto right now: Bitcoin ETFs just posted their worst month on record with $4.5 billion of outflows, Citi cut its 12-month inflow forecast to zero, and BTC sits near $64,000 — down from $93,000 in January. That is not automatically a buy signal. But it’s the exact opposite of priced for perfection — it’s priced for failure, and priced-for-failure is where homework pays the most. As we argued in The Fed Put Is Dead, the crowd’s positioning is usually the last thing to adjust to new data.

Third: let the punishment curve work for you. A -4.2% average miss penalty in a nervous, fully-valued market means volatility events are coming all season — good companies will get executed for one soft guidance line. If you keep a shopping list of businesses you’d love to own 15–20% cheaper and cash to act, this earnings season is a machine for delivering exactly those discounts. The investor who prepared the list in advance buys from the investor who bought perfection.

Wealth building has always been expectation arbitrage wearing a suit. Buy assets where reality has room to beat the assumptions. Sell — or at least stop adding to — assets where the assumptions have no room to be beaten. Right now the market is handing you a season-long, real-time map of which is which.

Want to track your own path to financial independence? The Wealtharian Wealth Tracker lets you monitor your net worth, FU money progress, and investment milestones in one place. Try it free →