TSMC just reported its fifth consecutive quarter of record earnings — profit up 77% year over year. The semiconductor index is down 20% from its highs anyway. Welcome to the first real AI correction: the strange, clarifying moment when the best earnings in the sector’s history meet a market that suddenly wants to talk about price.

If you own AI stocks — and if you own an index fund, you do — the last three weeks have felt like whiplash. Here’s the case that what’s happening is not the bubble bursting, but something more useful: the market is finally asking the right question. Not “is AI real?” but “who pays for it?” Getting that distinction right is worth more to your portfolio than any single stock pick this year.

Record profits, falling stocks

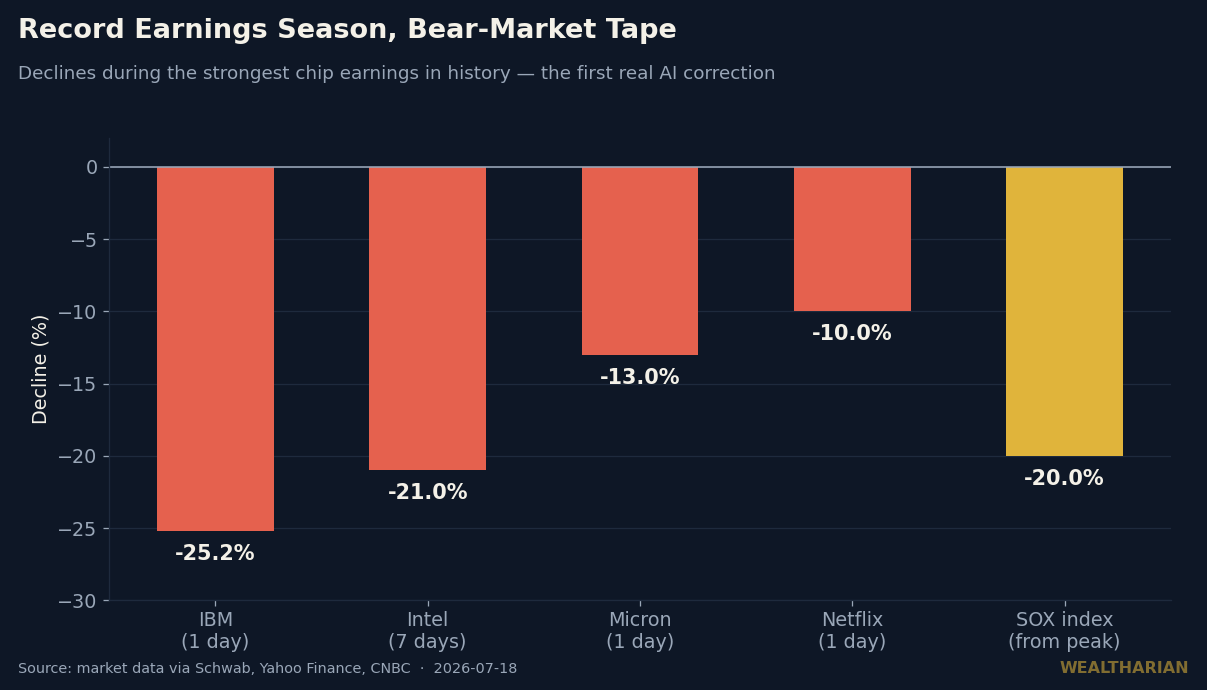

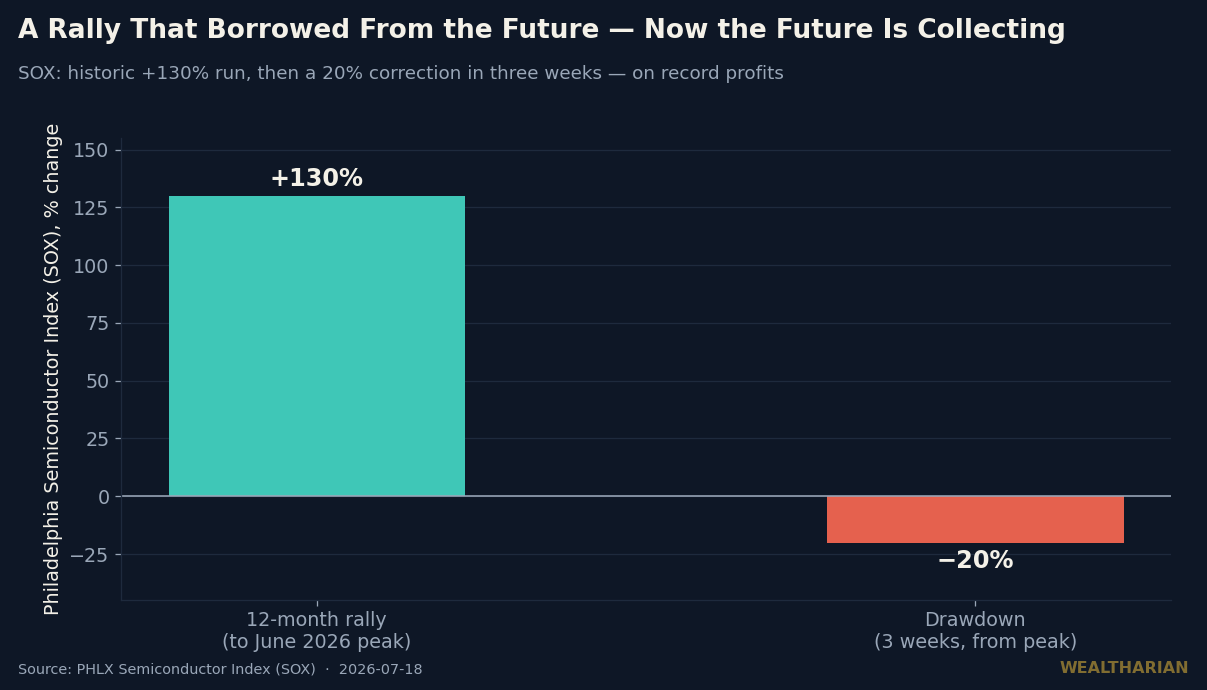

First, the scoreboard. On Friday the S&P 500 fell 1.0% to 7,457 and the Nasdaq dropped 1.4%, capping a week in which the Philadelphia Semiconductor Index reached roughly 20% below its recent highs — official correction territory, bordering on a chip bear market — after a historic 130% rally over the preceding twelve months. Intel lost 21% in seven trading days on reports its 18A-P foundry node won’t reach profitable yields until late 2026 or 2027. Micron shed 13% — about $38 billion — in a single session. Netflix fell 10% on a revenue miss measured in fractions of a percent.

Now the earnings those prices are reacting to. TSMC: fifth straight record quarter, profit up 77%. China’s AI chip supply chain: companies pre-announcing profit gains above 1,000% — and their stocks are mixed at best, because as Bloomberg dryly noted, investors had already priced in exponential growth. This is the same disease we diagnosed on Thursday in Priced for Perfection: when expectations are the price, even spectacular results stop paying. The AI trade has now caught it in its most acute form.

The IBM tell: AI isn’t new money

But the most important datapoint of the week — maybe of the AI era so far — wasn’t a chip stock at all. IBM fell 25.2% in one day. Its crime? Revenue of $17.2 billion, up just 1%. Investors looked at that number and reached a chilling conclusion: enterprise spending on chips, servers and AI infrastructure isn’t new budget. It’s coming out of the old budget — the software, consulting and services lines that companies like IBM have lived on for decades.

Read that again, because it rewrites the whole AI investment thesis. The bull case quietly assumed AI spending was additive — a new layer of demand on top of everything else. The IBM print says it’s substitutive: every AI winner has a donor. The trillions flowing into GPUs and data centers are being carved out of legacy IT, consulting hours, seat-based software licenses, and — eventually — headcount. The money comes from somewhere, and “somewhere” just reported earnings.

For investors this cuts both ways. It confirms AI demand is real and durable — companies don’t cannibalize their own IT budgets for a toy. But it also means the AI boom has a short side inside tech itself. The lazy trade was “buy tech, AI lifts all boats.” The correct trade is a pair: long the scarcity layer, short (or at least: not long) the donor layer — mature software vendors, IT consultancies, and anyone whose business model bills humans by the hour for work models are learning to do.

What an AI correction actually is

The word “correction” gets used loosely, so let’s be precise about what this one is and isn’t. The selloff was triggered by valuation and positioning, not by any collapse in demand: the catalysts were Meta announcing it will sell surplus AI compute (rewriting the supply-demand math for everyone renting it), Intel’s yield delays, and SK Hynix slowing HBM expansion — supply-side and price-side news, not “customers stopped buying.” Data-center demand forecasts are unchanged. TSMC raised its outlook and its capex the week chips fell hardest.

History’s most instructive parallel: Amazon fell roughly 90% between 2000 and 2001 while its revenue grew every single quarter. The internet thesis was right; the 1999 price was wrong. Investors who understood the difference — who staged into the correction instead of fleeing it or bottom-fishing it all at once — captured one of the great compounding runs of the century. A 130% rally in twelve months borrows returns from the future; a 20% drawdown is the future collecting. Neither tells you the technology failed.

The playbook for the drawdown

1. Buy scarcity, not activity. As we argued in The AI Picks-and-Shovels Trap, value pools where supply can’t respond quickly: advanced packaging, HBM memory (a three-company oligopoly), leading-edge foundry, grid power. In a correction, the scarce assets fall with the crowded ones — that’s the opportunity. The commodity layers fall for a reason.

2. Avoid the donors. Screen your portfolio for businesses on the paying side of the AI transfer: legacy enterprise software with per-seat pricing, IT services and consulting, business-process outsourcing. Their revenues are the raw material of the AI boom. IBM was a warning shot, not a one-off.

3. Stage in; don’t guess the bottom. Corrections inside secular trends historically reward scheduled, incremental buying over hero timing. Decide the total you’d deploy, split it into tranches, automate the tranches. Your edge is temperament, not telepathy.

4. Respect the macro overhang. Brent is near $87 on Middle East escalation, tanker traffic through Bab el-Mandeb has collapsed, and energy was the only green sector on Friday. An oil shock is the one macro force that could turn a valuation correction into an earnings problem. That’s an argument for dry powder, not for paralysis.

The first real AI correction is doing what corrections do: transferring shares from people who owned a story to people who own a framework. Record profits plus falling prices isn’t a contradiction — it’s an entrance exam.

Want to track your own path to financial independence? The Wealtharian Wealth Tracker lets you monitor your net worth, FU money progress, and investment milestones in one place. Try it free →